A Beginner’s Book on the Indian Taxation System

(Based on Latest Provisions Applicable for Assessment Year 2026-27)

Income tax is one of the most important subjects in financial literacy.

It affects individuals, businesses, investors, and governments.

भारत में Income Tax government revenue का एक प्रमुख स्रोत माना जाता है।

यह tax system national development को sustain करने में सहायता करता है।

Understanding income tax helps citizens plan finances responsibly.

यह knowledge taxpayers को compliance और financial planning में मदद करता है।

Accounting students, finance professionals और entrepreneurs taxation concepts regularly study करते हैं।

This guide is written in book format with chapters, illustrations, and examples.

Content structure beginners और accounting learners के लिए suitable है।

Chapter 1

Understanding Income: The Foundation of Taxation

Before learning taxation, we must first understand income.

Income refers to money earned through economic activity.

आय किसी व्यक्ति या संस्था द्वारा कमाया गया आर्थिक लाभ है।

यह salary, business profit, rent या investment return के रूप में प्राप्त हो सकती है।

Income increases financial capacity.

Therefore governments tax a portion of income.

Illustration

Suppose Rahul works in a private company.

Rahul earns ₹50,000 monthly salary.

यह amount उसकी employment income कहलाती है।

Rahul also earns ₹10,000 yearly bank interest.

अब उसकी total income multiple sources से आती है।

This total income becomes relevant for taxation.

Chapter 2

Meaning and Definition of Income Tax

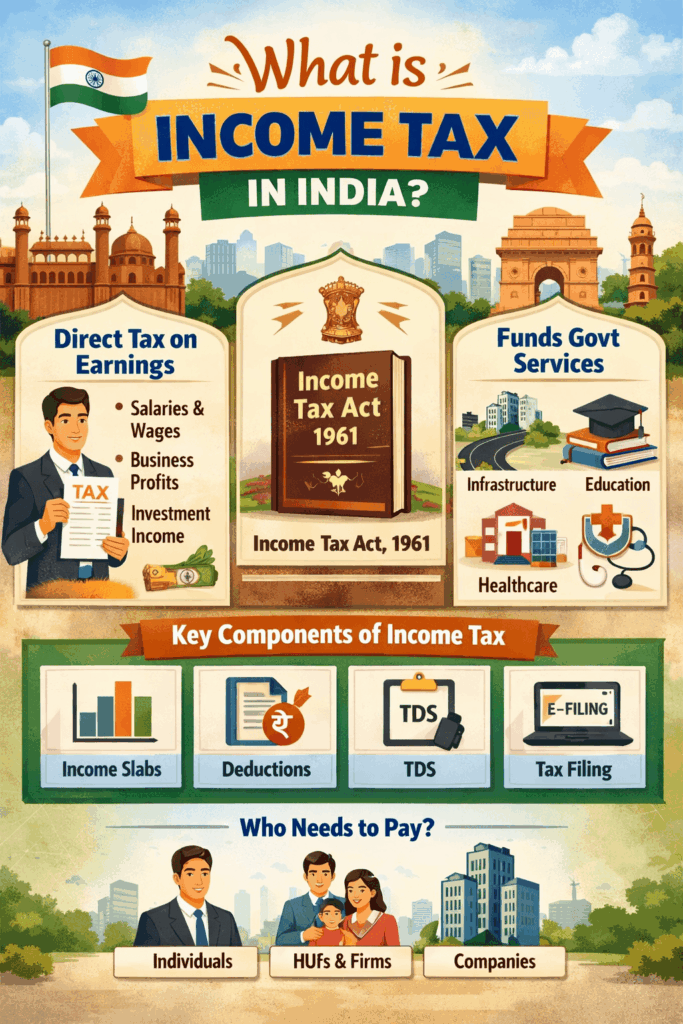

Income tax is a direct tax imposed on income earned by individuals or entities.

भारत में Income Tax government द्वारा लगाया गया प्रत्यक्ष कर है।

यह tax central government collect करती है।

The law governing income tax is the Income Tax Act 1961.

This act explains:

- taxable income

• exemptions

• deductions

• penalties

• compliance rules

Income tax is generally calculated annually.

Income earned during the financial year becomes taxable.

The next year is used for assessment.

Chapter 3

Objectives of Income Tax

Income tax fulfills several economic purposes.

The primary objective is government revenue generation.

Tax revenue public infrastructure development में invest किया जाता है।

Roads, bridges, airports और railways largely taxation funds से बनाए जाते हैं।

Income tax also promotes economic equality.

Higher income earners pay higher tax rates.

यह progressive taxation system कहलाता है।

Another objective is financial transparency.

Taxation system citizens को income reporting के लिए encourage करता है।

Chapter 4

Historical Development of Income Tax in India

Taxation in India has existed since ancient civilizations.

Ancient kingdoms collected taxes mainly on agriculture.

प्राचीन भारत में land revenue प्रमुख taxation source था।

Farmers produce का एक हिस्सा rulers को देते थे।

Modern income tax system British rule के दौरान introduced हुआ।

In 1860, the first income tax law was introduced.

Later reforms gradually modernized the system.

Finally the Income Tax Act 1961 became the main taxation legislation.

Today this act forms the backbone of India’s tax system.

Chapter 5

Basic Terminology Used in Income Tax

Taxation studies begin with understanding technical terms.

Assessee

Assessee वह person होता है जो tax pay करने के लिए liable है।

It includes individuals, companies, and organizations.

Person

Income tax law में “person” का meaning broader होता है।

It includes:

- Individual

• Hindu Undivided Family

• Partnership Firm

• Company

• Association of Persons

• Local Authority

All these categories fall under taxation rules.

Previous Year

Previous year refers to the income earning year.

Example:

Income earned during FY 2025-26 becomes taxable.

Assessment Year

Assessment year वह year होता है जिसमें income assessed की जाती है।

Example:

Income earned in FY 2025-26 is assessed in AY 2026-27.

Chapter 6

Residential Status and Tax Liability

Residential status determines taxation scope.

Income tax law taxpayers को residence criteria के आधार पर classify करता है।

Resident Individual

Residents pay tax on global income.

यदि foreign country से income earn की गई है, तब भी taxation applicable हो सकता है।

Non Resident Individual

Non residents Indian income पर tax pay करते हैं।

Foreign income usually taxable नहीं होता।

Resident but Not Ordinarily Resident

This category has limited taxation on foreign income.

Residential status tax liability calculation में significant role निभाता है।

Chapter 7

Heads of Income Under Income Tax Act

Income tax law income को five heads में classify करता है।

This classification helps systematic tax calculation.

1 Salary Income

Salary employer से received compensation होता है।

Components include:

- Basic salary

• Allowances

• Bonus

• Pension

Employers TDS mechanism के माध्यम से tax deduct करते हैं।

2 Income from House Property

Rental income property ownership से earn होता है।

Example:

A house rented for ₹20,000 monthly generates taxable rental income.

Housing loan interest deductions allowed होते हैं।

3 Profits and Gains from Business or Profession

Business income commercial activities से generate होता है।

Examples include:

- retail business profit

• consultancy income

• freelancing earnings

Business expenses taxable income से deduct किए जा सकते हैं।

4 Capital Gains

Capital gains assets sale से arise होते हैं।

Examples include:

- property sale

• shares sale

• mutual fund investments

Capital gains two types होते हैं:

Short term capital gains

Long term capital gains

5 Income from Other Sources

Certain incomes other heads में fit नहीं होते।

These incomes “Other Sources” category में taxed होते हैं।

Examples include:

- bank interest

• lottery winnings

• dividend income

Chapter 8

Income Tax Slabs in India (Latest for AY 2026-27)

India currently follows two tax regimes.

Taxpayers can choose between:

- Old tax regime

• New tax regime

The new regime is now the default system.

New Tax Regime Slabs (FY 2025-26)

Income up to ₹4 lakh → Nil tax

₹4 lakh to ₹8 lakh → 5%

₹8 lakh to ₹12 lakh → 10%

₹12 lakh to ₹16 lakh → 15%

₹16 lakh to ₹20 lakh → 20%

₹20 lakh to ₹24 lakh → 25%

Above ₹24 lakh → 30%

Key features include:

- Standard deduction ₹75,000

• Rebate up to ₹60,000

• Income up to ₹12 lakh effectively tax-free in many cases

Old Tax Regime Slabs

Up to ₹2.5 lakh → Nil

₹2.5 lakh – ₹5 lakh → 5%

₹5 lakh – ₹10 lakh → 20%

Above ₹10 lakh → 30%

However this regime allows deductions like:

- Section 80C

• HRA exemption

• Section 80D

• Housing loan interest

Chapter 9

Tax Deductions for Tax Planning

Deductions reduce taxable income legally.

They encourage savings and investments.

Section 80C

Maximum deduction allowed is ₹1.5 lakh.

Eligible investments include:

- Public Provident Fund

• Life Insurance

• Equity Linked Savings Scheme

• National Savings Certificate

Section 80D

Health insurance premium deduction allowed है।

Senior citizens higher deduction limits claim कर सकते हैं।

Housing Loan Deduction

Interest on housing loans deduction qualify करता है।

Maximum deduction usually ₹2 lakh तक allowed है।

Chapter 10

Income Tax Return Filing

Income tax return filing annual compliance requirement है।

Taxpayers earned income और paid taxes declare करते हैं।

India taxation system largely digital हो चुका है।

Online e-filing portal return submission simplify करता है।

Steps to File ITR

1 Calculate total income

2 Identify tax regime

3 Claim deductions

4 Calculate tax liability

5 Submit return online

Chapter 11

Illustrative Example of Income Tax Calculation

Suppose Meera earns ₹11,50,000 salary.

Standard deduction = ₹75,000.

Taxable income becomes ₹10,75,000.

Now tax is calculated under slabs.

After applying Section 87A rebate, tax liability becomes zero.

This happens because rebate up to ₹60,000 reduces tax.

Chapter 12

Importance of Income Tax Compliance

Tax compliance builds financial credibility.

Banks loan approval के समय tax returns verify करते हैं।

Visa applications में income tax returns useful documents होते हैं।

Tax revenue national development programs fund करता है।

Responsible taxpayers economic growth में contribution देते हैं।

Chapter 13

Future of Income Tax in India

India taxation system gradually digital transformation की ओर बढ़ रहा है।

Faceless assessment transparency improve करता है।

AI tools suspicious transactions detect करने में सहायता करते हैं।

Government simplified tax laws introduce करने का प्रयास कर रही है।

Future taxation system more transparent और efficient बनने की संभावना है।

Frequently Asked Questions

What is income tax in India?

Income tax individuals और entities की income पर लगाया जाने वाला direct tax है।

Which law governs income tax in India?

Income Tax Act 1961 taxation rules regulate करता है।

What is assessment year 2026-27?

यह year FY 2025-26 income assessment के लिए उपयोग होता है।

What is the new tax regime?

यह simplified taxation system है जिसमें lower rates लेकिन limited deductions होते हैं।

How much income is tax free in new regime?

Section 87A rebate के कारण ₹12 lakh तक taxable income effectively tax free हो सकती है।

Is income tax return filing compulsory?

Eligible taxpayers के लिए annual ITR filing mandatory होती है।

Chapter 14

Understanding Tax Deducted at Source (TDS)

Tax Deducted at Source is a system of collecting tax at the origin of income.

Income tax department ensures early tax collection through TDS.

यह system tax evasion को reduce करने में मदद करता है।

Under TDS, the payer deducts tax before making payment.

यह deducted tax government account में deposit किया जाता है।

Illustration

Suppose Ankit works in a company.

His monthly salary is ₹70,000.

Employer calculates annual income and applicable tax.

The employer deducts tax every month.

यह deduction salary slip में TDS के रूप में दिखाई देता है।

Example Calculation

Annual salary = ₹8,40,000

Standard deduction = ₹75,000

Taxable income = ₹7,65,000

Applicable tax is calculated according to slab rates.

Employer distributes this tax across twelve months.

Thus monthly TDS becomes approximately ₹2,500.

Chapter 15

Understanding Tax Collected at Source (TCS)

TCS refers to tax collected by sellers during transactions.

Certain goods transactions require sellers to collect tax.

भारत में TCS specific transactions पर लागू होता है।

यह tax seller buyer से collect करता है।

Examples include:

- scrap sale

• foreign remittance

• luxury goods purchases

• overseas travel packages

Illustration

Suppose a travel agency sells an international tour.

Tour cost = ₹3,00,000.

Applicable TCS rate = 5%.

Thus TCS collected = ₹15,000.

This tax is deposited with the government.

Chapter 16

Advance Tax System

Advance tax refers to paying tax before the end of the financial year.

Income tax law requires taxpayers to pay tax in installments.

यदि total tax liability ₹10,000 से अधिक है, advance tax applicable हो सकता है।

Advance tax is paid in four installments.

Due Date | Tax Percentage |

15 June | 15% |

15 September | 45% |

15 December | 75% |

15 March | 100% |

Case Illustration

Rohit runs a small consultancy business.

Estimated annual tax liability = ₹80,000.

He must pay advance tax installments according to schedule.

Chapter 17

Understanding Capital Gains

Capital gains arise when a capital asset is sold at profit.

Assets include property, shares, bonds, and mutual funds.

जब asset की selling price purchase price से अधिक होती है, capital gain उत्पन्न होता है।

Capital gains taxation depends on holding period.

Types of Capital Gains

Short Term Capital Gain

Asset held for shorter period.

Higher tax rates generally apply.

Long Term Capital Gain

Asset held for longer duration.

Lower tax rates usually apply.

Illustration

Purchase price of shares = ₹1,00,000.

Selling price after 1 year = ₹1,40,000.

Capital gain = ₹40,000.

Applicable capital gains tax will apply.

Chapter 18

Indexation in Capital Gains

Indexation adjusts purchase price for inflation.

This reduces taxable capital gains.

Inflation increases asset prices over time.

Indexation helps maintain fairness in taxation.

Example

Property purchase price in 2010 = ₹20,00,000.

Indexed value in 2025 becomes higher due to inflation.

Tax is calculated on adjusted gain.

Thus tax burden reduces significantly.

Chapter 19

Concept of Goods and Services Tax (GST)

GST is an indirect tax introduced in India in 2017.

It replaced multiple indirect taxes.

GST consumption based tax system है।

Consumer final tax burden bear करता है।

Businesses collect GST and deposit it to government.

Chapter 20

Difference Between Income Tax and GST

Income tax and GST are different taxation systems.

Feature | Income Tax | GST |

Type | Direct tax | Indirect tax |

Who pays | Income earner | Consumer |

Collected by | Central government | Centre and states |

Applicable on | Income | Goods and services |

Both taxes contribute to national revenue.

Chapter 21

Tax Planning vs Tax Evasion

Tax planning means reducing tax legally.

Tax evasion means avoiding tax illegally.

Legal tax planning allowed होता है।

Examples include:

- investment under Section 80C

• health insurance deduction

• retirement savings

Tax evasion may lead to penalties.

Chapter 22

Permanent Account Number (PAN)

PAN is a unique identification number for taxpayers.

PAN financial transactions track करने में मदद करता है।

Every taxpayer must obtain PAN before filing returns.

Banks, employers, and financial institutions require PAN.

Chapter 23

Aadhaar and Income Tax

Aadhaar linking improves transparency in taxation.

Income tax return filing में Aadhaar authentication required हो सकता है।

This reduces duplicate identities and fraud.

Chapter 24

Income Tax Return Forms

Different taxpayers file different ITR forms.

Common forms include:

ITR-1 → salaried individuals

ITR-2 → individuals with capital gains

ITR-3 → business income taxpayers

ITR-4 → presumptive taxation scheme

Correct form selection ensures accurate return filing.

Chapter 25

Presumptive Taxation Scheme

Presumptive taxation simplifies tax calculation for small businesses.

Small taxpayers simplified method use कर सकते हैं।

Instead of detailed bookkeeping, fixed percentage income assumed होता है।

Sections applicable include:

- Section 44AD

• Section 44ADA

Example:

Professional income ₹10 lakh.

50% income assumed taxable.

Tax calculated on ₹5 lakh.

Chapter 26

Penalties and Compliance

Income tax law imposes penalties for non compliance.

Late return filing may attract fees.

Interest may apply on unpaid taxes.

Serious violations prosecution cause कर सकते हैं।

Timely filing ensures smooth compliance.

Chapter 27

Faceless Assessment System

India introduced faceless tax assessment system.

This reduces human interaction in tax scrutiny.

Transparency increases and corruption reduces.

Digital communication improves efficiency.

Chapter 28

Tax Audits

Tax audit verifies accuracy of financial records.

Businesses above certain turnover limits require audit.

Audit ensures correct income reporting.

Chartered accountants usually conduct tax audits.

Chapter 29

Case Study: Salary Income Calculation

Rahul earns ₹12,50,000 salary annually.

Standard deduction = ₹75,000.

Taxable income becomes ₹11,75,000.

Slab based tax calculation applies.

After rebate adjustments, final tax becomes minimal.

This demonstrates practical tax computation.

Chapter 30

Case Study: Business Income Tax Calculation

A freelance designer earns ₹9,00,000 annually.

Using presumptive taxation under Section 44ADA:

50% income assumed taxable.

Taxable income = ₹4,50,000.

Tax liability becomes very small due to rebates.

This scheme simplifies tax compliance.

Chapter 31

Case Study: Rental Income

Priya owns an apartment rented for ₹25,000 monthly.

Annual rent = ₹3,00,000.

Standard deduction under house property = 30%.

Taxable rental income becomes ₹2,10,000.

Tax calculated accordingly.

Chapter 32

Case Study: Capital Gain Calculation

Raj purchased land for ₹10,00,000.

After 5 years he sells it for ₹18,00,000.

Capital gain = ₹8,00,000.

After indexation adjustment taxable gain reduces.

This lowers tax liability.

Chapter 33

Digital Tax Ecosystem in India

India taxation system rapidly digitalizing हो रहा है।

Online portals simplify compliance.

Taxpayers file returns electronically.

Digital records reduce errors and fraud.

Chapter 34

Future Trends in Taxation

Future taxation may include greater automation.

Artificial intelligence will detect suspicious transactions.

Simplified tax structures may emerge.

Government continues improving transparency.

IPA offers Tax Consultant Course & Income Tax Practitioner Course in Delhi

6/mar/62/ia

References

Income Tax Act 1961

Central Board of Direct Taxes publications

Union Budget 2025 tax provisions

Ministry of Finance India reports

Sanjeev Malik is a taxation trainer and accounting educator with experience in GST, income tax, and financial compliance training. He teaches practical accounting, taxation, and GST courses to students and professionals in India. He is the founder of IPA – The Institute of Professional Accountants , where students learn GST filing, income tax return preparation, and accounting software.

Connect with him through the following platforms:

Institute Website: www.tipa.in